Grow revenue faster with seamless physical and virtual card issuing.

Feature-rich card experiences.

Card Token Management

Push Provisioning

Mastercard Smart Data

Instant Issue

ATMs

3D Secure

High Interchange

Variable Interchange

Multi-Currency BINs

Rewards

Deposit Sweeps

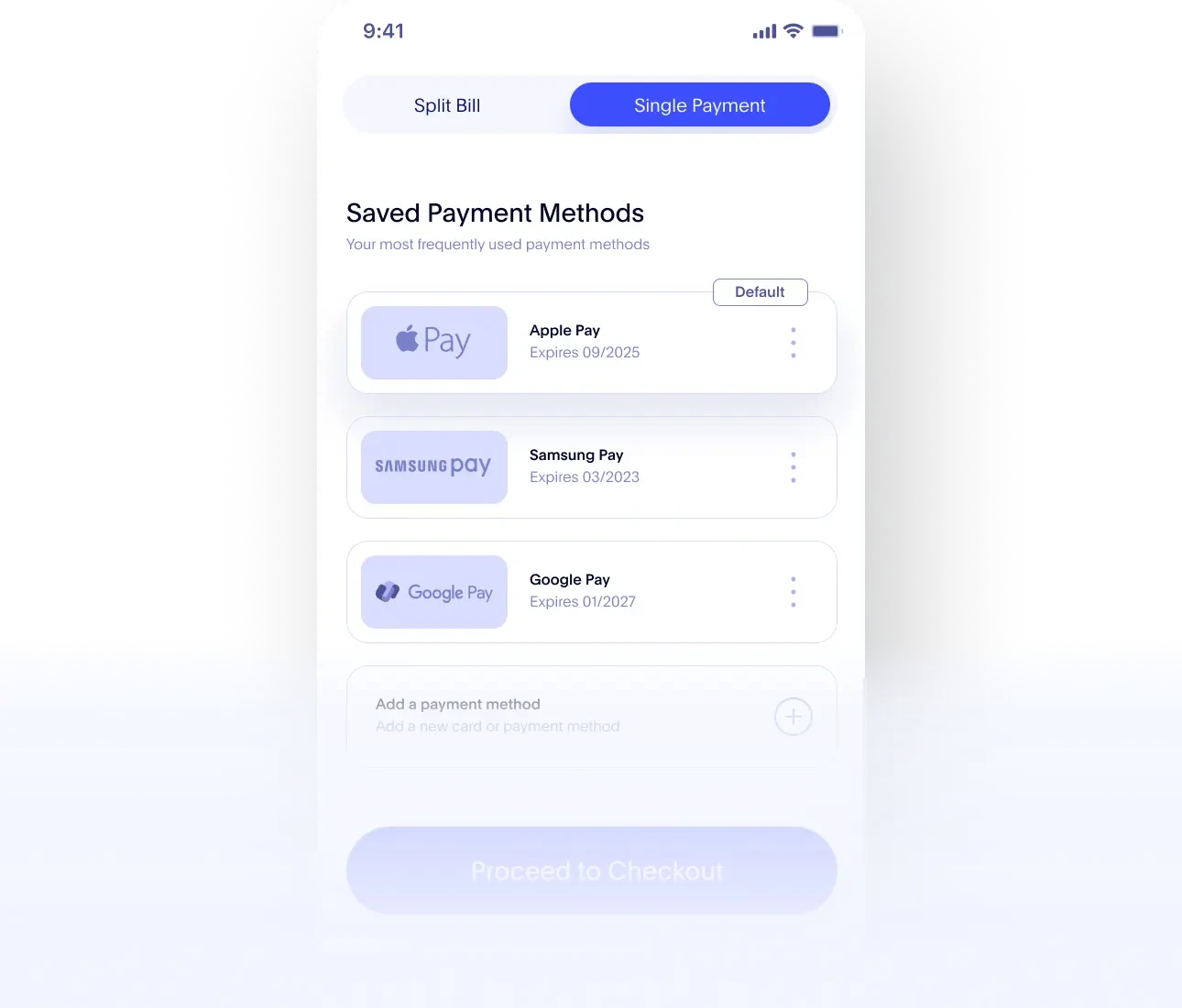

Digital First

Round Up

Real-Time Funding

Corporate Hierarchy

Galileo named Best-in-Class for digital issuance.

Consumer, small business and commercial cards.

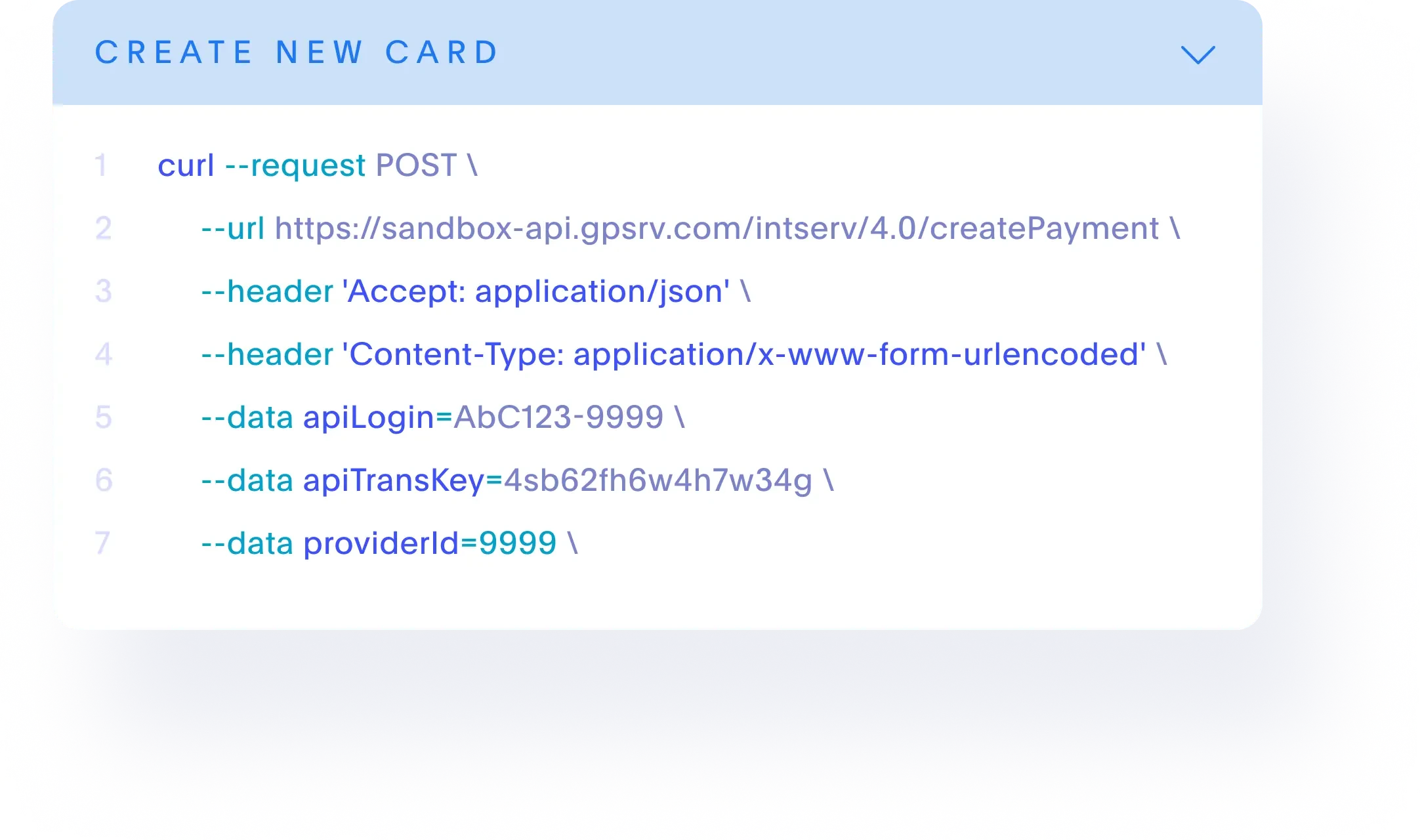

Issue payment cards with confidence.

Our payments experts guide you through each step of your program setup, from program integration to card distribution. Whether it’s EMV chip or contactless cards, building brand value and customer loyalty starts with card issuing done right—fast, seamless and secure.

We enable instant issue of virtual accounts to generate account numbers for cardholders in real time.

Take the complexity out of card issuing.

Learn how our solutions can elevate your offerings with a personalized self-guided demo of our APIs.

Go digital-first with one-click push provisioning.

Protect every transaction with advanced authentication.

3D Secure (3DS) adds an extra layer of security to online card payments—helping companies prevent fraud, protect customers, and increase transaction approval rates. With built-in authentication tools, 3DS helps verify cardholder identity in real time without disrupting the checkout experience.

- Frictionless authentication for trusted customers and transactions

- Dynamic fraud prevention with risk-based decisioning

- 3D Score insights to optimize approval rates and reduce fraud risk

Tap into our extensive integrated payment network.