Aumente a receita mais rapidamente com a emissão de cartões físicos e virtuais sem complicações.

Experiências de cartão ricas em recursos.

Gerenciamento de Tokens de Cartão

Provisionamento Push

Mastercard Smart Data

Emissão Instantânea

Caixas Eletrônicos

3D Secure

Alto Intercâmbio

Intercâmbio Variável

BINs Multimoeda

Recompensas

Sweep de Depósitos

Digital First

Arredondamento

Financiamento em Tempo Real

Hierarquia Corporativa

Galileo é nomeado Melhor da Categoria em emissão digital.

Cartões para consumidores, pequenas empresas e corporativos.

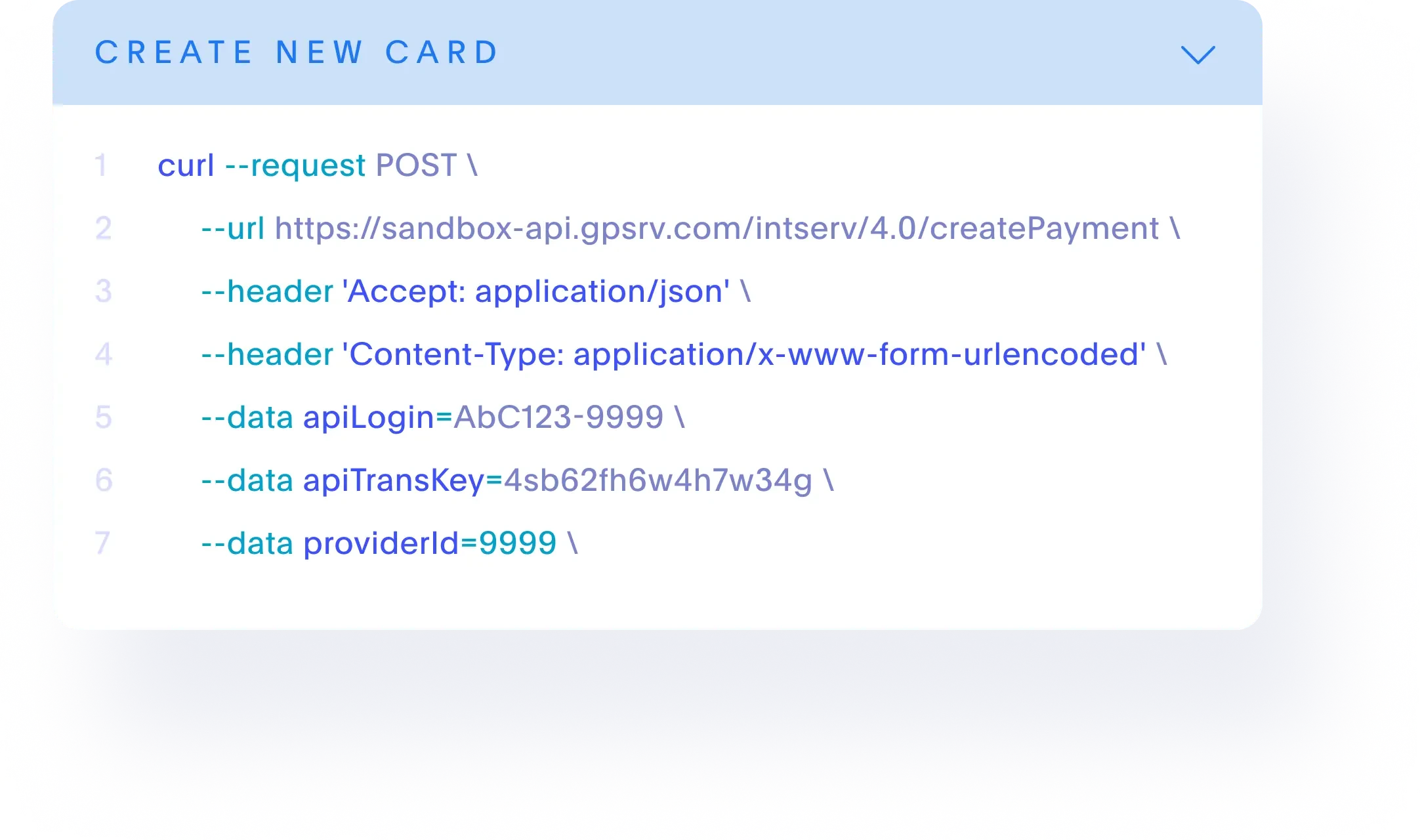

Emita cartões de pagamento com confiança.

Nossos especialistas em pagamentos orientam você em cada etapa da configuração do seu programa, desde a integração até a distribuição dos cartões. Seja com cartões com chip EMV ou por aproximação, agregar valor à marca e fidelizar clientes começa com uma emissão de cartões feita da maneira certa — rápida, sem complicações e segura.

Permitimos a emissão instantânea de contas virtuais para gerar números de conta em tempo real para os titulares de cartões.

Elimine a complexidade da emissão de cartões.

Learn how our solutions can elevate your offerings with a personalized self-guided demo of our APIs.

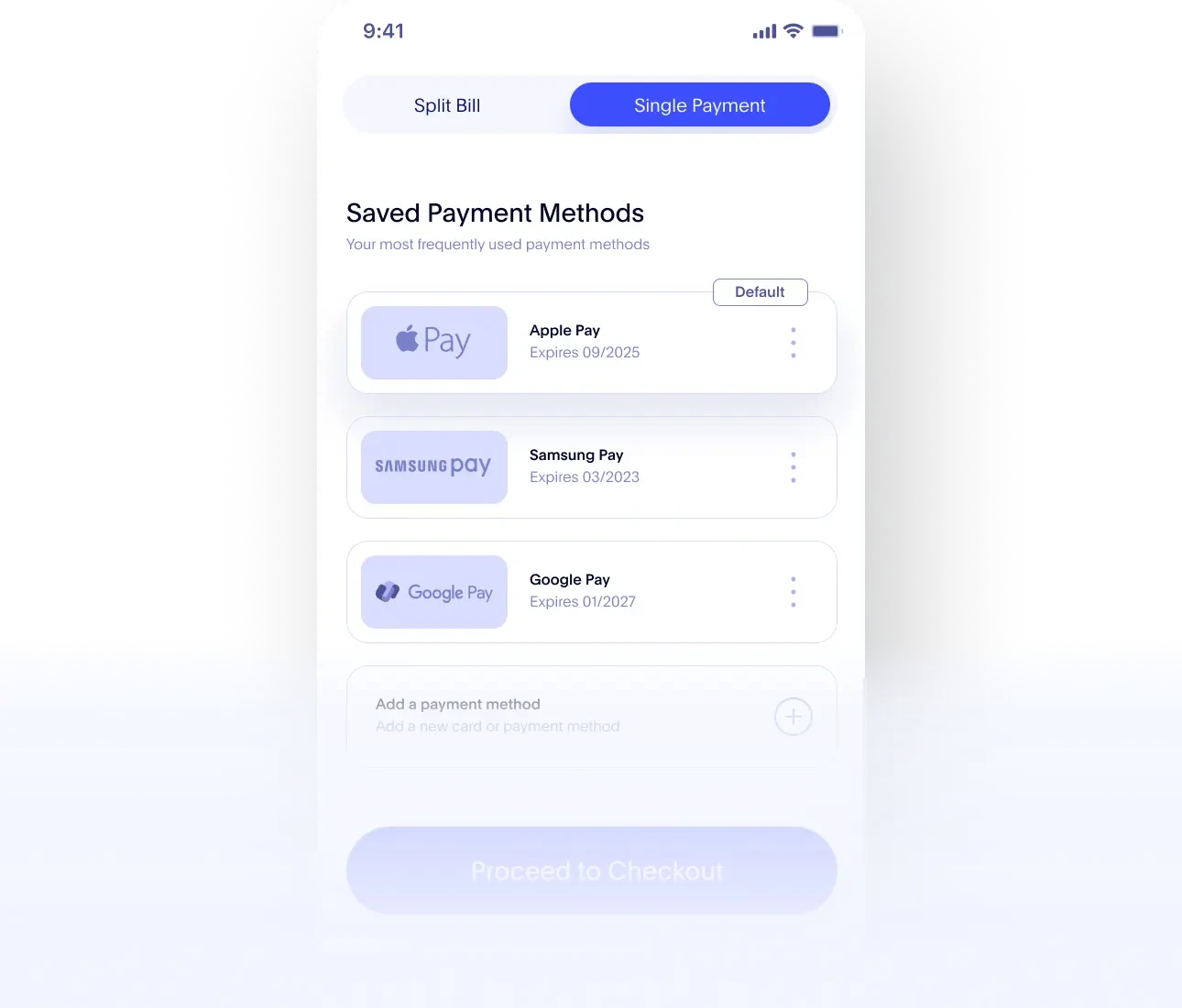

Vá direto ao digital com o provisionamento push com um clique.

Proteja cada transação com autenticação avançada.

O 3D Secure (3DS) adiciona uma camada extra de segurança aos pagamentos com cartão online—ajudando as empresas a prevenir fraudes, proteger clientes e aumentar as taxas de aprovação de transações. Com ferramentas de autenticação integradas, o 3DS ajuda a verificar a identidade do titular do cartão em tempo real sem interromper a experiência de checkout.

- Autenticação sem fricção para clientes e transações confiáveis

- Prevenção de fraude dinâmica com decisões baseadas em risco

- Insights do 3D Score para otimizar taxas de aprovação e reduzir o risco de fraude

Acesse nossa extensa rede de pagamentos integrada.