CYBERBANK CORE

Future-ready scalability for your bank.

Modernize your banking operations with Cyberbank Core—a next-generation, cloud-native platform designed to accelerate innovation, enhance customer experiences and boost operational efficiency.

NEXT-GEN CORE BANKING

Full-stack Gen 3.0 banking solution when combined with Digital.

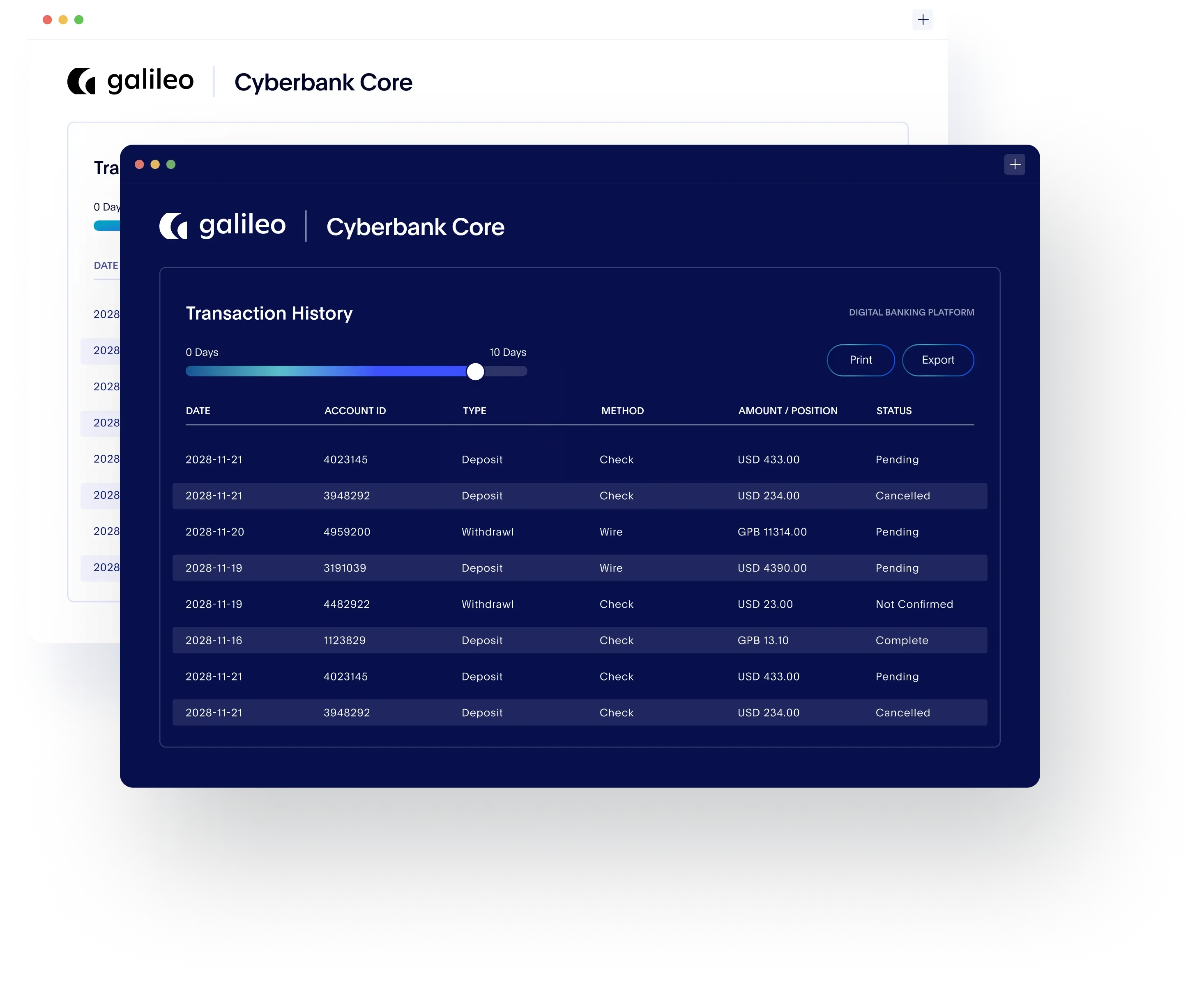

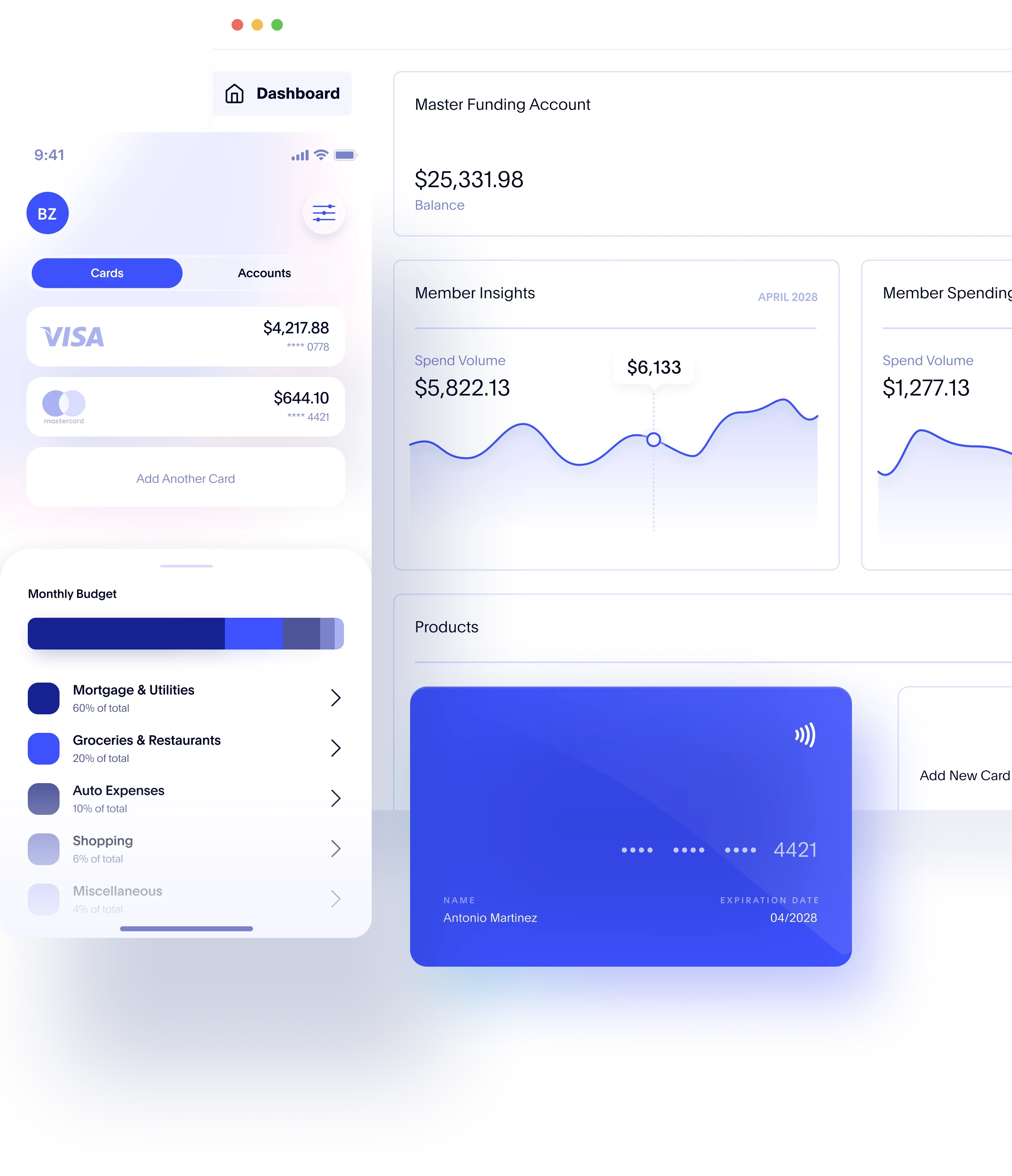

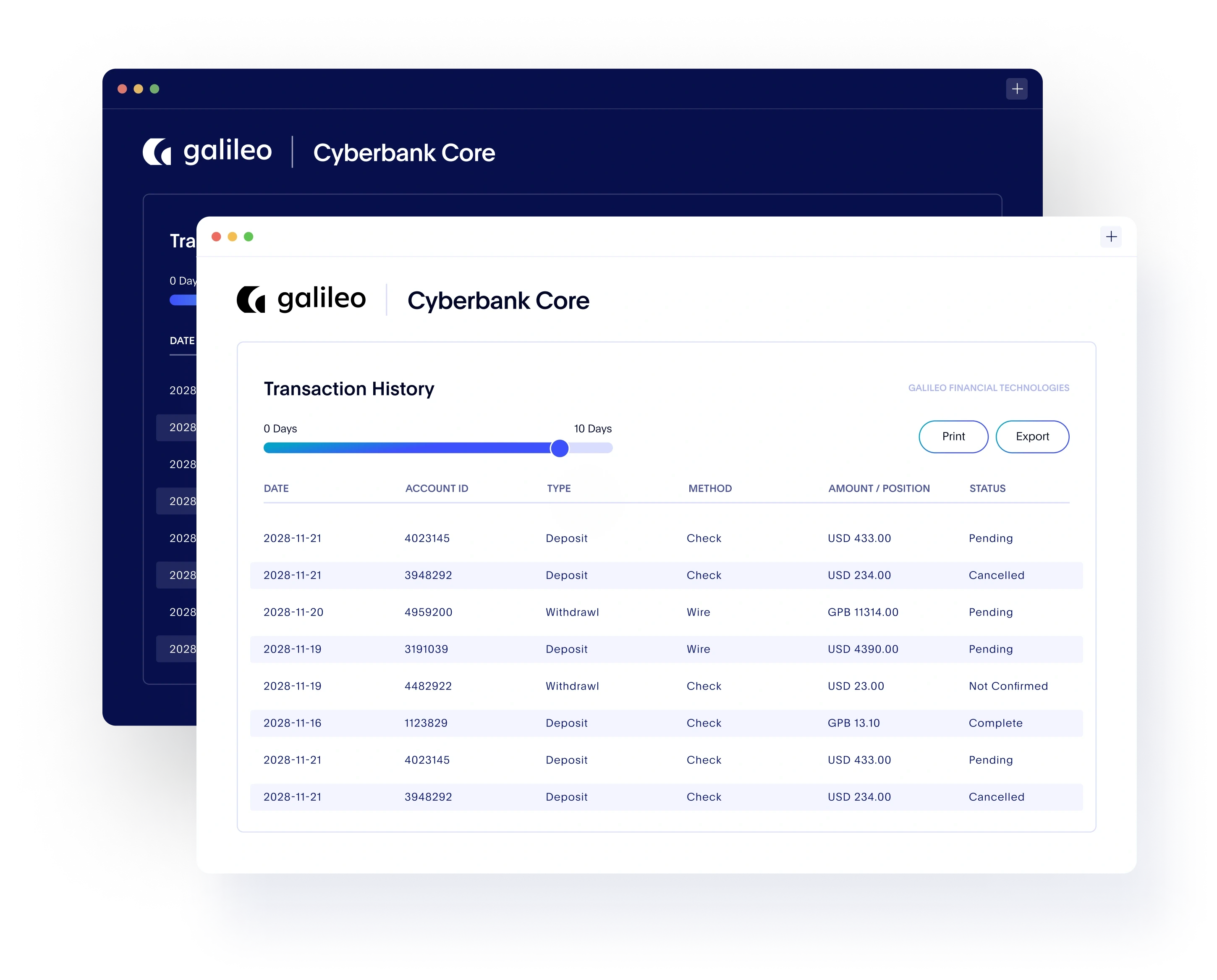

Cyberbank Core is a modern, API-first core banking platform designed to enable financial institutions and banks to deliver innovative, customer-centric financial solutions. Built for scalability, flexibility, and rapid integration, Cyberbank Core unites deposits, loans, and payment services to replace outdated systems which can scale to more than 10,000 Transactions Per Second without sacrificing performance.

Empowering banks to innovate faster, integrate seamlessly and scale effortlessly.

THE "CORE" PROBLEM

Traditional core systems often struggle with limitations such as lack of agility, high operational costs, and challenges in integrating with emerging technologies or third-party solutions.

TAILORED PRODUCTS

Cyberbank Core addresses these issues by providing an API-first, modular platform that streamlines operations, enhances product innovation, and delivers seamless customer experiences.

The Solution

By replacing rigid legacy systems, Cyberbank Core enables banks to rapidly launch new financial products, scale operations, and seamlessly integrate with third-party ecosystems, ensuring they stay competitive in an ever-evolving financial landscape.

Learn more about Cyberbank Core.

.avif?u=https%3A%2F%2Fimages.ctfassets.net%2Fbvz14004tu0h%2F1VhxM2exKd5xJSst9ytkTi%2Fae125ef7d62d11d9e1b4f2e230433d98%2FSoFi_to_Adopt_Galileo-s_Cyberbank_Core_for_Sponsor_Banking__1_.png&a=w%3D1200%26h%3D675%26fm%3Davif%26q%3D75&cd=2024-10-15T19%3A26%3A16.159Z)

The Future of Banking

Build the future of banking with Cyberbank Core.

We’ll help you deliver seamless, personalized, and innovative financial experiences your customers will love.